Applicazione di richiesta di informazioni sulla regolamentazione dei broker globali

WikiFX

English

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

What Drives a Gold Bear Market?

Sommario:According to the World Gold Councils journal, a historical review of the past five gold bear markets highlights the key risks that could drive medium-term corrections in the future.Nov 1974 – Aug 1976

According to the World Gold Councils journal, a historical review of the past five gold bear markets highlights the key risks that could drive medium-term corrections in the future.

Nov 1974 – Aug 1976, return -43%; Reason: easing geopolitical risks

Aug 1980 – Jun 1982, return -52%; Reason: easing geopolitical and inflation risks

Jan 1983 – Feb 1985, return -57%; Reason: easing geopolitical and economic risks

Nov 1987 – Aug 1999, return -48%; Reason: central bank gold sales, increased supply

Aug 2011 – Dec 2015, return -42%; Reason: declining risks and weakening momentum

The study suggests that major gold corrections are largely linked to a rise in opportunity costs, particularly when real interest rates and the U.S. dollar strengthen.

At times, this is fueled by economic expansion; at others, by rapid Fed rate hikes. Higher opportunity costs and robust economic performance tend to dampen investor appetite for gold while boosting risk-on sentiment.

(Figure 1. Gold Drawdowns vs. Real Rates & USD; Source: World Gold Council)

Structural Shifts Since 2000

Since 2000, gold has only experienced one bear market, largely due to three structural shifts:

Strong economic expansion, with surging demand from emerging markets such as China and India.

A reversal in central bank behavior—from net sellers over two decades to net buyers after 2009, making a significant contribution to annual demand.

The creation and rapid growth of global gold ETFs, attracting a new wave of investors.

Scenarios for Long-Term Weakness

Central Bank Exit

If major buyers such as central banks were forced to liquidate reserves due to fiscal or economic crises, global trade contraction, or shrinking FX reserves, demand for gold could sharply decline—even turning negative. This would remove a critical layer of market support.

Cryptocurrency Boom

Should digital assets gain formal recognition from leading economies, with new regulatory frameworks driving institutional adoption, gold‘s role as a reserve asset could weaken. If the U.S. were to establish official crypto reserves, both investors and central banks could divert allocations away from gold.

Capital Market Liberalization

If countries like China and India fully open their capital markets, gold’s role as a global safe-haven asset may diminish. A generational shift in consumer preferences—where younger demographics lose interest in gold jewelry—would further weaken both investment and consumption demand.

Excess Supply from Major Discoveries

The discovery of large, economically viable gold deposits could trigger a supply surge. If production costs remain low and labor is concentrated, expanded supply could rebalance the market for decades.

Conclusion

Technical Analysis

If gold were to undergo a longer-lasting downturn, structural shifts like these would need to reverse. Simply put, a true gold bear market would most likely be driven by competition from alternative assets that better match evolving investor preferences.

From the current macro and industry perspective, the three largest gold miners have not significantly increased capital expenditures, instead maintaining a cautious stance despite higher prices. Meanwhile, market liberalization in major economies like India and China remains a long-term probability rather than an immediate threat.

Thus, we do not expect structural headwinds for gold at this stage. However, our bearish view is currently anchored on two key factors: the repatriation of U.S. dollars and the growing role of cryptocurrencies in global reserves.

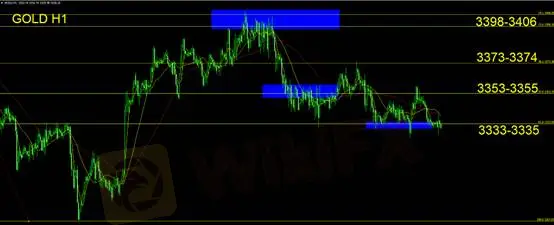

Gold reversed downward from the $3,353–$3,355 resistance zone and broke below the $3,333–$3,335 support during todays Asian session, confirming that bearish momentum remains intact. Investors should continue to favor short positions.

For existing shorts: consider setting stop-loss at breakeven.

For new entries: initiate short positions in the $3,333–$3,335 range with a stop-loss of $15.

Support: $3,333–$3,335

Resistance: $3,353–$3,355 / $3,373–$3,374 / $3,398–$3,406

⚠ Risk Disclaimer

The above analysis, research, prices, and commentary are provided solely as general market insights and do not represent the stance of this platform. Market participants assume full responsibility for their investment decisions. Please trade with caution.

Disclaimer:

Le opinioni di questo articolo rappresentano solo le opinioni personali dell’autore e non costituiscono consulenza in materia di investimenti per questa piattaforma. La piattaforma non garantisce l’accuratezza, la completezza e la tempestività delle informazioni relative all’articolo, né è responsabile delle perdite causate dall’uso o dall’affidamento delle informazioni relative all’articolo.

WikiFX Trader

Plus500

Sotto supervisione

octa

Sotto supervisione

InteractiveBrokers

le lista nera

FXCM

Sotto supervisione

Vantage

Sotto supervisione

D prime

Sotto supervisione

Plus500

Sotto supervisione

octa

Sotto supervisione

InteractiveBrokers

le lista nera

FXCM

Sotto supervisione

Vantage

Sotto supervisione

D prime

Sotto supervisione

WikiFX Trader

Plus500

Sotto supervisione

octa

Sotto supervisione

InteractiveBrokers

le lista nera

FXCM

Sotto supervisione

Vantage

Sotto supervisione

D prime

Sotto supervisione

Plus500

Sotto supervisione

octa

Sotto supervisione

InteractiveBrokers

le lista nera

FXCM

Sotto supervisione

Vantage

Sotto supervisione

D prime

Sotto supervisione

Rate Calc

USD

CNY

Tasso di cambio attuale: 0

inserisci l'importo

USD

A disposizione

CNY

Calcolare